- COVID-19 cases top 220 million worldwide with a confirmed case fatality rate of ≈2.1% and an estimated infection fatality rate of ≈0.7%.

- Novel mRNA vaccines developed in record time by Pfizer-BioNTech and Moderna with ≈95% vaccine efficacy against the original ‘wild’-type virus.

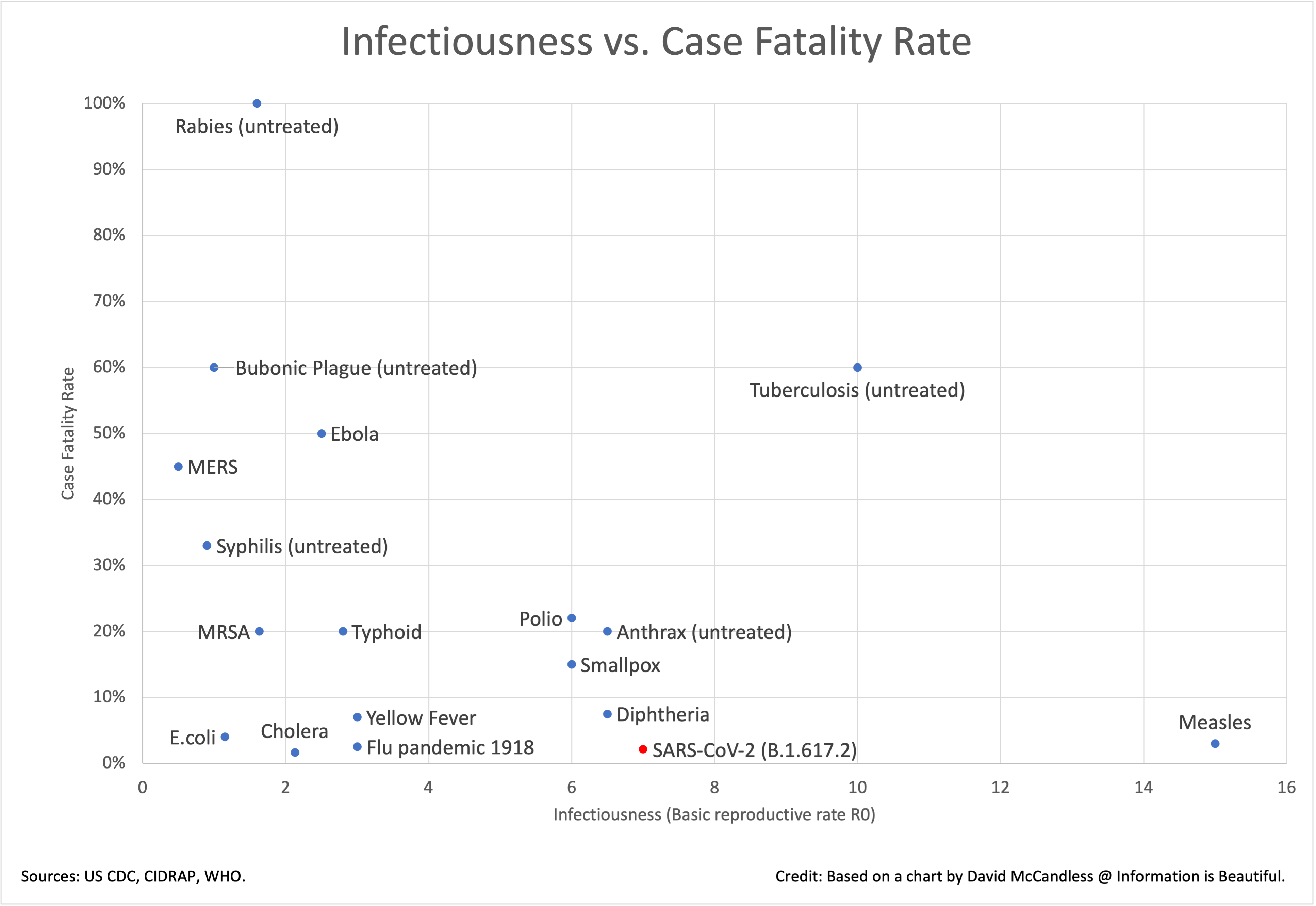

- Highly transmissible SARS-CoV-2 Delta variant emerges, with key reproductive number R0 estimated at between 6 and 7, making Delta as infectious as smallpox.

- Multiple countries hit by repeated pandemic waves with global hotspots currently including Israel, Malaysia, the UK, and the US Deep South.

- 5.2 billion vaccine doses administered to date in a race against the Delta variant as 40% of the world’s population receives at least one dose of a COVID-19 vaccine.

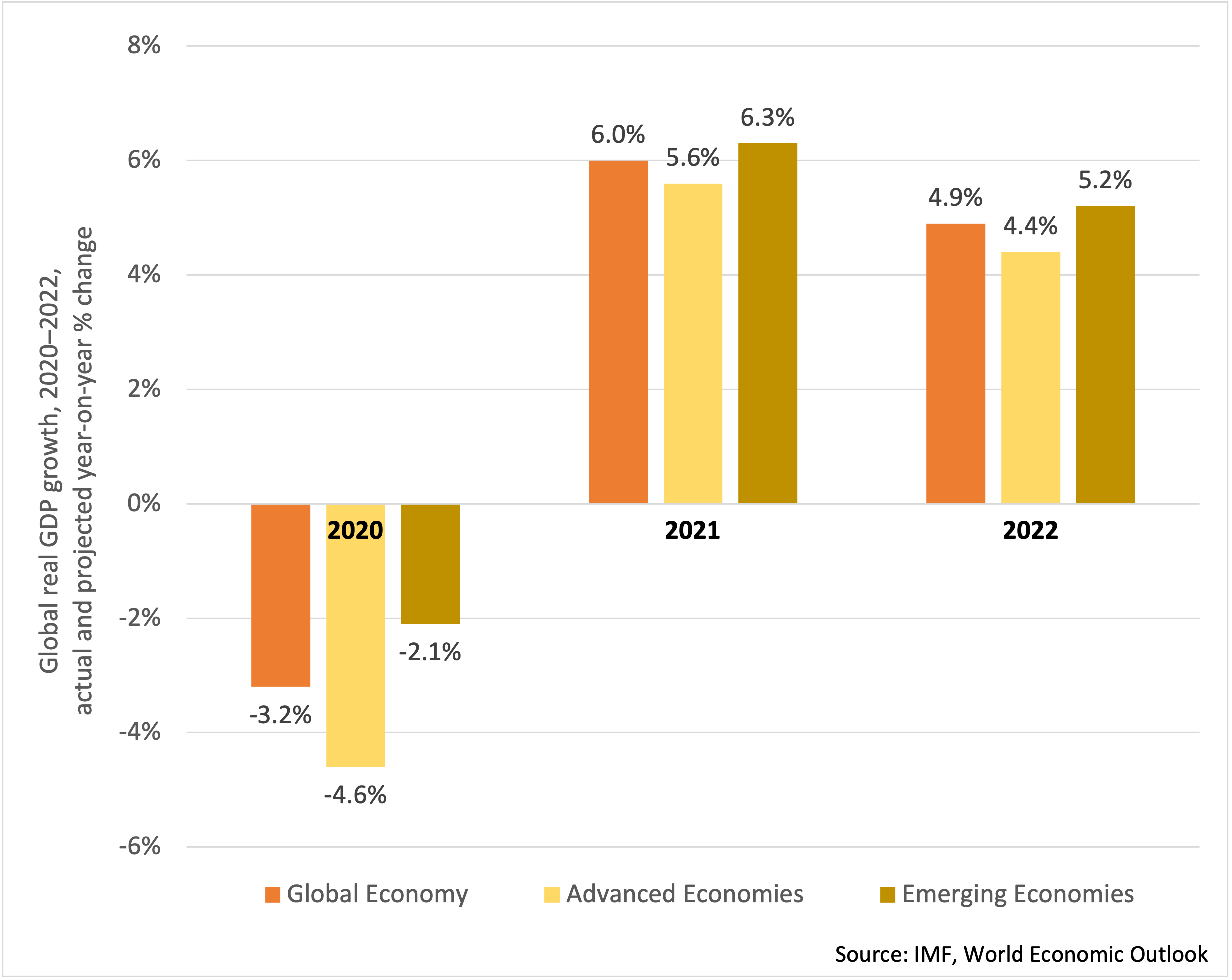

- IMF forecasts global real GDP growth of 6% in 2021 and 4.9% in 2022 on the back of a vaccine-powered recovery.

- Lotteries rebound after a turbulent 2020, with H2GC estimating 5.3% growth to date in 2021.

- The world turns to digital, with H2GC reporting growth in interactive of 37.4% to date in 2021 as land-based gaming declines 19.1% over the corresponding period.

- H2GC now projecting total global gross win returning to pre-pandemic levels by end 2022.

In this special edition of the WLA Quarterly Lottery Sales Indicator, we report once more on the rapidly unfolding regional and worldwide developments in the fight against COVID-19, and the impact of the pandemic on the lottery industry globally. Initially, the collective response to the pandemic consisted largely of a rolling series of lockdowns across the globe to ‘flatten’ the epidemiological curve. These lockdowns, while imposed at a tremendous cost to societal wellbeing and economic activity, were essentially the only effective public health mitigation then available in the absence of vaccines. In a triumph of modern medicine, and just over a year after the first documented case of COVID-19, the US Food and Drug Administration (FDA) issued the first Emergency Use Authorization (EUA) for a COVID-19 vaccine, engineered by Pfizer-BioNTech, on 11 December 2020. This was followed a week later by a second EUA for Moderna’s COVID-19 vaccine. EUAs for further vaccines such as the one-shot Janssen COVID-19 vaccine (Johnson & Johnson) followed.

With primary efficacy analysis of Phase III clinical trials demonstrating the Pfizer-BioNTech and Moderna COVID-19 vaccines to be 94% or better effective against the original ‘wild’ strain of COVID-19, it appeared for a short interval that the advent of good vaccines would soon bring the pandemic to a comparatively swift conclusion, at least across North America and Europe. However, the emergence of the SARS-CoV-2 Delta variant (B.1.617.2) in late 2020 dashed such hopes. Being at least 50% more transmissible than the original ‘wild’ strain of the SARS-CoV-2 virus, exhibiting some vaccine escape, and appearing to have more serious consequences for those infected – especially children – transmission rates have continued to climb, even as significant populations across Europe and North America have been inoculated. Indeed, Figure 1 reveals that SARS-CoV-2 B.1.617.2 is one of the most contagious respiratory viruses ever known. With worldwide daily cases at the time of writing now at almost 80% of their all-time peak despite aggressive vaccination campaigns (see Figure 2), many epidemiologists believe the pandemic still has some distance to run.

Figure 1. Comparison of SARS-CoV-2 (Delta variant) to common infectious diseases.

Figure 2. Daily new confirmed cases and total confirmed cases of COVID-19 globally through to August 2021.

Some eighteen months into the pandemic, a clearer picture is now beginning to emerge of the impact of the global contagion on the lottery and gaming sector. At the time of last writing, the entire gaming sector had been hit by an unprecedented triple whammy that saw entire populations going into lockdown, the postponement or cancellation of major sports events including the Tokyo Olympics and EURO 2020, and widespread disruptions to retail networks through enforced closures of non-essential businesses. Following this early turmoil, the entire lottery and sports betting sector regrouped and recovered. The sector moved aggressively to online, optimized retail sales channels otherwise, and innovated game content through new product launches and via the additions of extras and asides to existing brands. In short, the industry has generally responded to the global health crisis with verve, creativity, and elan. Some of the trends now emerging and conclusions that may be tentatively drawn include:

- To the end of financial year 19/20 or calendar year 2020, most lotteries experienced considerable initial disruption, followed by recovery to near pre-pandemic performance.

- For the financial year 20/21 or calendar year beginning in 2021, most lotteries have enjoyed substantial growth, sometimes to record levels of lottery sales.

- There has been a significant and sustained uptake of iGaming and other online products, with digital typically experiencing 30 to 40% growth year-on-year. This has been accompanied by a concomitant decline in land-based gaming, with casinos particularly badly hit.

- Increased personal income, especially in the US, together with fewer opportunities to spend disposable income (owing to lockdowns and other pandemic restrictions), has been a key driver of growth in some markets and for some verticals.

- The desire to fortify sales mid-pandemic has driven both new and existing game development, engendering many new innovations like the UK National Lottery’s ‘Must Be Won’ roll-down draws for its Lotto flagship. Such innovations have typically been enthusiastically welcomed by players.

- It is not yet clear whether the recent increase in play above traditional levels will be maintained post-pandemic. Sustaining current levels of lottery sales may depend upon maintaining lottery as an attractive alternative, apropos (5) above, as the currently restricted field of entertainment options recovers.

In the sequel, we take a closer look at points (1)–(6) above for some of the world’s major lottery and sports betting entities (and a smattering of smaller operators) across Africa, Asia Pacific, Europe, and Latin America, setting their operations and pandemic response in the context of current local conditions. For North America, where the state-based system gives rise to many operators, we consider the market both as a whole and by vertical, highlighting the performance of individual state lotteries on occasion as appropriate.

Africa

Daily new confirmed COVID-19 cases per million people in Africa at end August 2021, 7-day rolling average. (The number of confirmed cases is lower than the number of actual cases owing to limited testing.)

The novel coronavirus initially spread more slowly in Africa than in any other region of the world. However, the continent is now in its third and worst wave of the pandemic, with major outbreaks in both the north (Tunisia, Egypt, Morocco) and south of the continent (South Africa). South Africa remains the continent’s most badly impacted country, although the picture is not completely clear owing to a likely undercounting of cases, hospitalizations, and deaths across much of Africa. Vaccination rates across the continent remain low, even in the continent’s most developed nation, South Africa.

South Africa

South Africa, with more than 2.8 million confirmed cases of COVID-19 and more than 81,000 deaths, has borne the brunt of the impact of COVID-19 on the African continent to date, at least according to official figures. In South Africa, a national state of disaster was declared on 15 March 2020, with an initial three-week nationwide lockdown commencing 26 March; this was subsequently extended to the end of April 2020. A ZAR 500 billion economic stimulus package followed to support the economy during the quarantine period. Lockdown restrictions were lifted in phases, with restrictions relaxed to level one (the lightest) in September 2020. A second and worse wave of the pandemic began in December 2020; lockdown restrictions were tightened to level three, and were not relaxed to level one again until March 2021. The country’s vaccination program officially began on 17 February 2021. Local cases of the Delta variant were first identified in May 2021, and on 8 June South Africa entered level four lockdown restrictions (the next-to-most most severe) in response to a third (Delta-driven) wave. In July, CNN reported that the country’s hospital situation was under seriously challenged, and in August Bloomberg reported that South Africa’s economy was likewise under severe strain, with the jobless rate surging to 34.4% in the second quarter of 2021.

The financial year ending in March 2021 was thus by far the most challenging that ITHUBA – the proud operator of the South African National Lottery – has had to face, given the impact of the global pandemic on the company’s business model and the wider economy. Prior to March 2021, ITHUBA had successfully enjoyed record-breaking years in each of its years of operation. The company has operated the South African National Lottery since 2015 and offers a wide range of fun, safe, and entertaining games for public consumption, including draw-based games (Lotto, Powerball), instants (EaziWin), and sports betting (SportStake). Draw-based games compose approximately 95% of the market.

For FY 20/21, ITHUBA reported an overall decline in sales of 8.5%, versus the previous financial year. Chief Executive Officer of ITHUBA, Charmaine Mabuza remarked that the FY 20/21 results were very commendable given the extreme impact of COVID-19, which included both periods of hard lockdown and a total ban on lottery ticket sales in retail stores during May 2020.

Indeed, the hard lockdowns forced all non-essential businesses to vacate their facilities and operate remotely, which for ITHUBA included all draw procedures. Fortunately, ITHUBA had previously migrated to an electronic drawing system (RNG) and animated draw shows, so the lottery was able to adapt to a fully remote draw procedure very quickly, continuing operations throughout the lockdown periods. To this day the remote working model remains in operation with all draws conducted remotely and with most staff working from home. Overall, sales of draw-based games were down 8.1% financial year on financial year. As retail sales dropped, ITHUBA was able to compensate by increasing sales on-line through its banking partner Apps and through its eCommerce web site, mobile channels, and Lottery App. Currently, ITHUBA sells some 40% of lottery games through digital channels.

Instant games were removed from retail stores in response to the trend towards on-line sales and the preference of retailers to remove paper and minimize COVID-19 risks at the point of sale. COVID-19 restrictions limited the number of players and shoppers in stores at any one time and for certain periods casinos and smaller gaming houses were forced to close along with liquor stores, further curtailing lottery retail activity. Owing to these and other measures, instant sales decreased 26.9% financial year on financial year. Sports Pool games were also disrupted by the lack of available football fixtures in H1 2020, only returning to normality later in that year. Sales of sports betting products ultimately fell by 12% for FY 20/21, as against FY 19/20.

Commenting on the lottery’s performance, Chief Executive Officer of ITHUBA, Charmaine Mabuza said, “Despite the challenging year that was 2020/21, our performance has once again exceeded expectations. ITHUBA is proud of the flexibility and agility of its systems and staff to respond to the global pandemic positively and productively.”

Asia Pacific

Daily new confirmed COVID-19 cases per million people in Asia Pacific at end August 2021, 7-day rolling average. (The number of confirmed cases is lower than the number of actual cases owing to limited testing.)

Asia Pacific has continued to be more successful than many other parts of the world in its response to the COVID-19 pandemic, perhaps thanks to previous experiences with the SARS epidemic of 2002-2003 and the outbreak of MERS in Korea in 2015. China, Hong Kong, and South Korea have had ongoing success in curtailing the spread of the SARS-CoV-2 virus through a combination of aggressive containment measures, universal masking, comprehensive track and trace programs and quarantine measures, and public buy-in. New Zealand, which has followed a ‘zero-COVID’ approach, has almost completely suppressed the virus; the same too could be said for Australia, until a recent outbreak of the infectious Delta variant emerged in Sydney in June 2021. A notable exception to these success stories has been India, which was badly blighted by COVID-19 in a long six-month wave that commenced late February 2021. Somewhat surprisingly, vaccine rollouts across Asia Pacific have been uneven, even in developed countries like Australia and Japan.

China

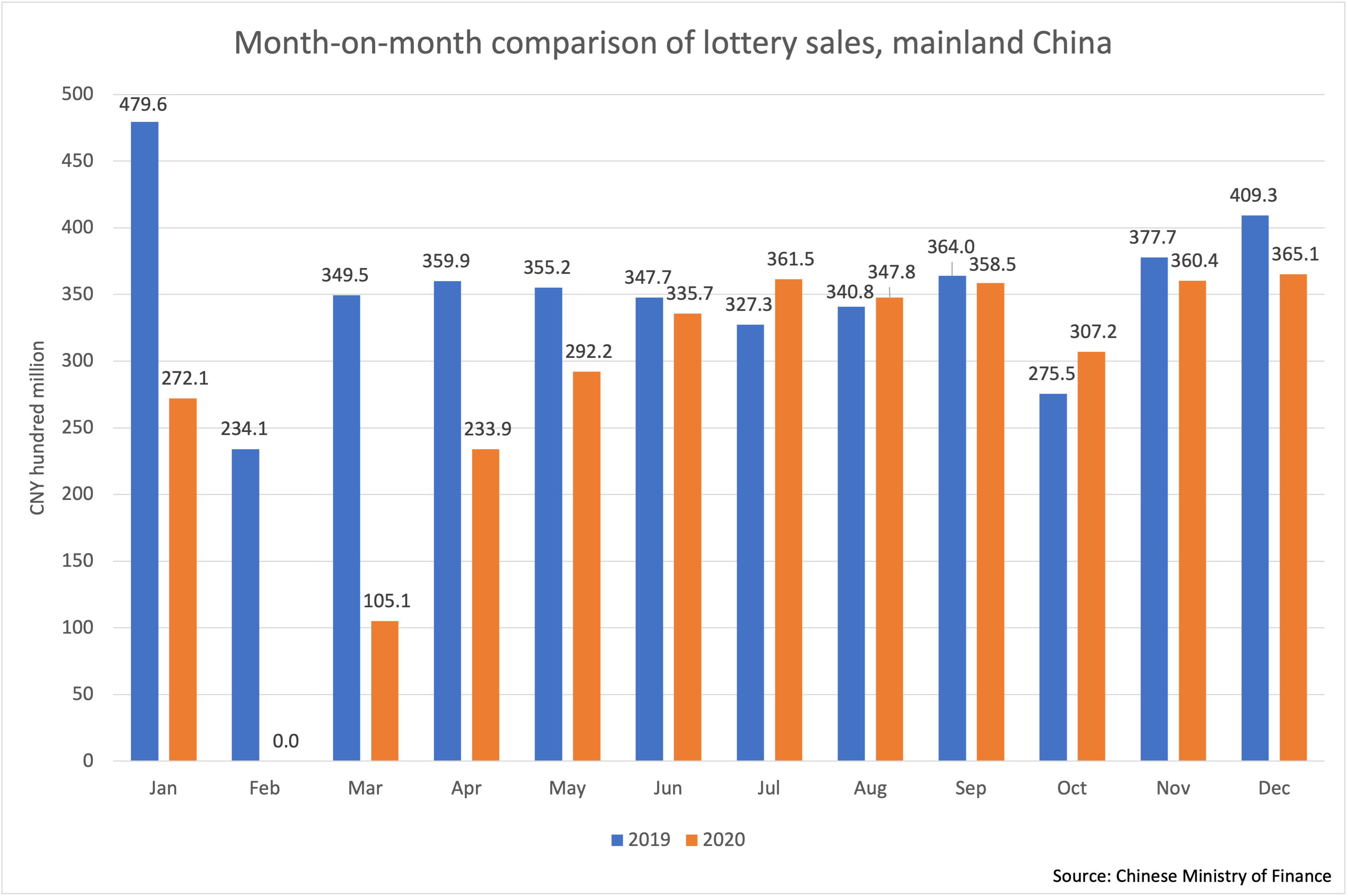

Lottery operations across mainland China were hit hard during the first three months of 2020, as Figure 3 shows. Recall that, owing to the national response to the COVID-19 pandemic, lottery retailer business hours were severely curtailed in February 2020; this, together with the 49-day suspension of lottery operations (including a 10-day shutdown over the Spring Festival holiday) mandated from 22 January 2020 ensured sales came to a standstill. Draws for national lotto and numbers games did not resume until 11 March, and VLT halls re-opened only on 11 May.

Figure 3. Month-on-month comparison of lottery sales across mainland China, 2020 vs. 2019.

With the gradual reopening of the lottery market in mainland China from March onwards, sales at the two mainland state lotteries began to rebound, especially in the second half of 2020, when revenues began to approach pre-pandemic levels. Whereas sales of lottery products decreased 64.5% across mainland China during Q1 2020, as compared to the corresponding revenue period of 2019, by Q4 2020 revenues were down only 2.8% on Q4 2019 revenues, with sales in October 2020 actually peaking sales in October 2019. Overall, lotteries in mainland China closed out 2020 with total sales of CNY 333.95 billion, a year-on-year decrease in sales of CNY 88.1 billion, or 20.9%. From January 2020 through to December 2020, sales at the China Welfare Lottery were CNY 144.49 billion, a year-on-year decline of CNY 46.8 billion, or 24.4%. Over the same period, sales at the China Sports Lottery were CNY 189.5 billion, a year-on-year decrease of CNY 41.4 billion, or 17.9%.

Owing to the closure of lottery operations across mainland China in Q1 2020, plus various other special factors such as policy adjustments impacting the market, lottery sales across mainland China in Q1 2021 are not directly comparable to sales across Q1 2020. Nonetheless, total revenues from lottery sales across mainland China amounted to CNY 84.5 billion for the first three months of 2021.

Turning attention to H1 2021, lottery sales increased rapidly over the period January – June 2021, as against the period January – June 2020, owing to the artificially depressed sales of the first three months of 2020, as occasioned by the COVID-19 pandemic. For the first six months of 2021, total sales of lottery products nationwide amounted to CNY 178.4 billion, an increase of CNY 54.5 billion, or 44.0% year-on-year. The China Sports Lottery carried the bulk of the increase, with sales at China Sports coming in at CNY 110.7 billion over the first half of 2021, an increase of CNY 46.1 billion over H1 2020, or 71.4%. For its part, the China Welfare Lottery reported sales of CNY 67.7 billion over the first six months of 2021, an increase of 14.2% or CNY 8.4 billion over the corresponding revenue period of 2020.

Market changes

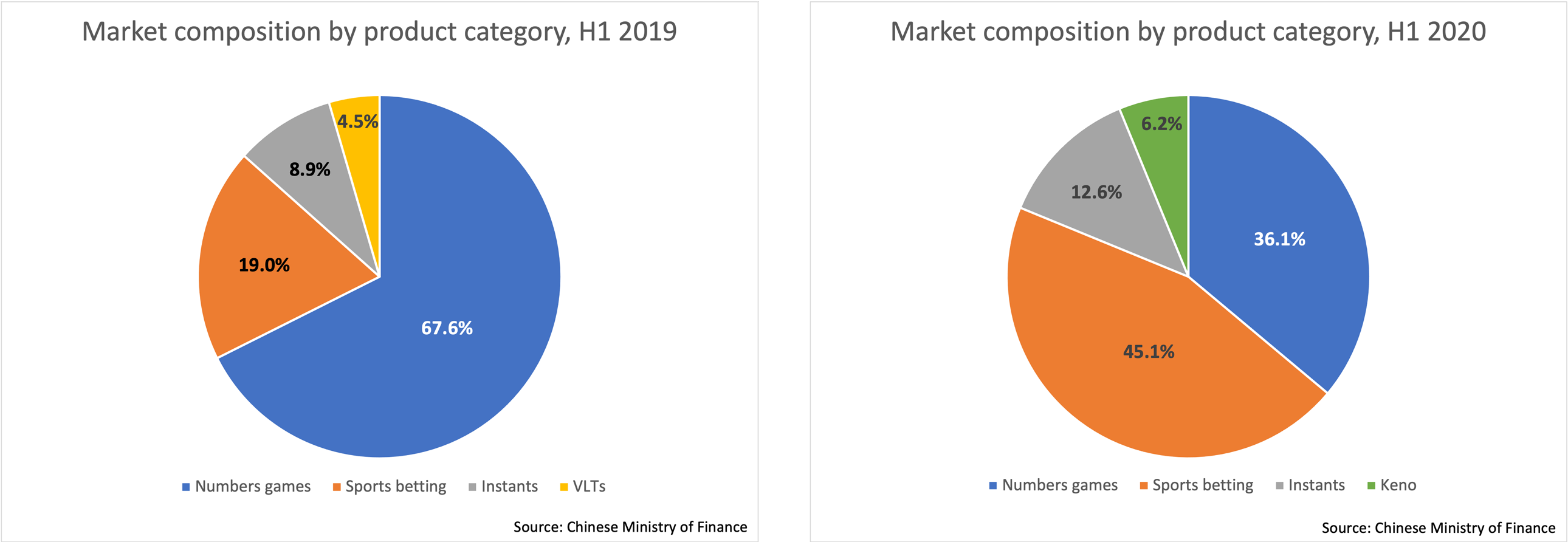

Beyond the upheaval caused by the COVID-19 pandemic, lottery sales across mainland China in 2021 were impacted by a number of procedural and policy changes, including: the suspension of certain online video lottery games; rule changes in particular Keno games, expansion of the scope of sales; the delisting of some high-frequency lottery games; and other factors such as the adjustment and optimization of lottery product structures. In sum, the sales of major lottery products have fluctuated significantly year-on-year. Thus, for example, sales of numbers games accounted for 67.6% of the market in June 2020, but only 36.1% of the market in June 2021; in this connection, see Figure 4. In general, the market share of numbers games decreased from 72.7% in the first half of 2020 to 47.1% in the first half of 2021, while sports betting sales increased from 13.8% market capture to 33.5% market capture over the same year-on-year timeframe.

Figure 4. Change in composition of the Chinese lottery market (mainland China) by product category, June 2020 vs. June 2021.

Hong Kong, China

Hong Kong, China, has had a very successful response to the pandemic to date, reporting just over 12,000 confirmed COVID-19 cases and only 212 deaths; the special administrative region’s comparatively flat epidemiological curve is especially remarkable give Hong Kong’s status as an international transport hub. Academic observers attribute Hong Kong’s success in fighting the pandemic to early and aggressive mitigation efforts on both public health and economic fronts – especially during the first wave of the pandemic – together with the universal masking habits adopted by Hong Kong residents since the territory’s previous experience in battling the SARS epidemic of 2003. A mild second wave was followed by a more serious third wave in August 2020, attributed to imported cases; this was followed by a comparatively severe fourth wave that began in November 2020. A series of partial lockdowns, targeted down to the residential level, mass testing, and a free mass vaccination program (from early 2021) were successfully used to curtail the spread of the virus, and since May 2021 Hong Kong has been averaging less than seven new cases of COVID-19 per day.

FY 20 results

The Hong Kong Jockey Club (HKJC), which was recently named most attractive employer in Hong Kong by international human resources solutions agency Randstad in a 2021 employer brand research survey, has main product offers of horse race betting, football betting, and the Mark Six lottery. It was the Mark Six lottery that bore the brunt of the impact of the COVID-19 pandemic on HKJC in 2020, with lottery draws being suspended between February and mid-September 2020 for public health reasons. Accordingly, Mark Six lottery sales fell 39% year-on-year to HKD 5.2 billion for the fiscal year ending in June 2020. Sales of fixed odds sports betting products were also adversely affected, with FY 20 stakes declining 18.8% year-on-year to HKD 92.6 billion owing to the absence of international football fixtures. Only pari-mutuel horse race betting weathered the initial storm of COVID-19, with FY 20 stakes decreasing only slightly, down 2.6% year-on-year to HKD 121.6 billion. In a testament to the business’ resilience, horse racing continued uninterrupted throughout the 2019/20 racing season thanks to stringent admission arrangements to control attendance and mitigate health risks trackside. Overall, turnover fell 11.3% year-on-year to HKD 219.4 billion.

FY 21 results

The challenges presented by the pandemic notwithstanding, HKJC set a new turnover record of HKD 279.7 billion for the financial year through to June 2021. This enabled the Club to make a significant return to the community of HKD 29.4 billion. Transfers to beneficiaries included a record HKD 24.9 billion to the Hong Kong government in duty, profits tax, and Lotteries Fund contributions. The Club’s Charities Trust also approved HKD 4.5 billion in charity donations, matching the previous year’s record high. HKJC’s impressive FY 21 results were predicated on guiding principles established by the Club at the beginning of the pandemic, namely that nothing it does should create a public health risk and that nothing should put the health and safety of the Club’s employees and customers at risk. The success of Club’s pandemic response was further underpinned by its ongoing business development.

Over the course of the 2020/21 racing season, HKJC enjoyed an all-time turnover record of HKD 136 billion (USD 17.5 billion). This is the first time in HKJC’s history that turnover has exceeded HKD 130 billion. HKJC was able to successfully progress the 2020/21 racing seas by creating a protective ‘racing bubble’ at its Sha Tin and Happy Valley racecourses. Accordingly, the Club limited racecourse attendance and closed or provided limited services at Off-Course Betting Branches and Telebet. The ‘racing bubble’ strategy was so successful that not a single race was lost throughout the season, and indeed the LONGINES Hong Kong International Races was the only international sporting event in held in the special administrative region in 2020. Overall, racing turnover for the season grew 12.1% year-on-year. Commingling, by which means the Club taps the rich potential of overseas markets, contributed some 17% of overall racing turnover. In support, the number of racing simulcast days was increased from 23 to 37 per year by the Hong Kong government. The 206 simulcast overseas races were yet another record for the Club.

The Mark Six Lottery, which only fully resumed over-the-counter sales in May 2021, saw sales decrease by 34% year-on-year. Compared against FY 19 lottery sales, lottery revenues are down by more than half overall. In contrast, sports betting was up significantly for FY 21, with revenues increasing 51.4% year-on-year to HKD 140.2 billion, reflecting both the resumption of the major football leagues from the second half of 2020 and the realization of postponed matches and competitions, including EURO 2020 and the Copa America 2020. The resulting situation with its exceptionally large number of football fixtures is unlikely to reoccur. Compared to FY 19, the most recent year with a regular football schedule, sports betting revenues were up 23% overall.

Given the ongoing impact of COVID-19, HKJC’s support for the community has been more important than ever. Its record-equaling donations of HKD 4.5 billion in FY 21 notwithstanding, the Club’s Charities Trust has approved HKD 1.5 billion in specific pandemic relief measures since February 2020, with more than a million people benefiting to date.

Digital transformation

The Club’s strong financial performance over the past year owes a great deal to the success of its digital products, with over 90% of wagering turnover in FY 21 being generated via online and mobile channels. Accordingly, the digital transformation of the Club’s wagering services continues apace. New products launched in FY 21 included a football app, an eWallet to facilitate cashless betting in Off-Course Betting Branches, and secure online account opening.

Macau, China

In the special administrative region of Macau, China, casinos predominate; Macau overtook the Las Vegas strip in terms of gaming revenues in 2007. One of the world’s strictest border control regimes has kept COVID-19 infections to just 63 confirmed cases to date in the former Portuguese colony, but has also devastated revenues: Macau’s GDP, which depends heavily on taxes on gaming, declined 56% to USD 24 billion in 2020. Currently, Macau monthly visitor numbers remain deeply depressed. Pre-pandemic, Macau received more than three million visitors monthly on average; current footfall is less than one million visitors per month. The impact of COVID-19 on gaming in Macau is a microcosm of the virus’ impact on gaming more generally, with H2GC reporting that gaming in Asia Pacific is down by 21.9% in 2021 to date and 20.9% globally.

Australia

Until very recently, Australia has been comparatively unaffected by the SARS-CoV-2 pandemic, thanks largely to a ‘zero-COVID’ strategy pursued aggressively by the premiers of the various Australian states and territories. However, with the advent of the Delta variant, the state of New South Wales has been experiencing (by Australian standards) a major outbreak since June 2021, with Australia’s most populous state currently experiencing around 1,000 new confirmed cases a day. Fortified by its earlier successes in tackling the pandemic, Australia has been comparatively slow getting its vaccination program off the ground – it is ranked close to last in vaccine uptake among OECD countries – with the unfortunate result that the country’s largest city, Sydney, now faces a period of extended lockdown to curtail the virus’ spread. Two million people are currently under curfew.

Tabcorp Holdings Limited is Australia’s largest gaming operator, operating state-regulated lotteries in all of Australia’s states except Western Australia. The group operates three business units: lotteries and Keno; wagering and media; and gaming services. Here we report on overall group and lottery and keno results only. For FY 19/20, overall group revenue was down 4.8% to AUD 5,224 million owing to the impact of COVID-19, even as Australia was comparatively lightly impacted by COVID-19 restrictions during the reporting timeframes. During this period lotteries exhibited strong performance, with like-for-like sales up circa 15 to 30% during COVID-19 restrictions. Overall lotteries and Keno revenues were AUD 2.9 billion, up 1.8% year-on-year; despite strong digital performance, Keno full-year revenues were down 14.3% on the back of enforced closures of clubs and hotels in New South Wales, Victoria, and Queensland during the second half of 2020. While the retail network – including newsagents and convenience stores – largely continued trading during the COVID-19 lockdown periods, retail turnover declined 4% in FY 20. In contrast, digital turnover grew strongly, accounting for 28% of total lotteries turnover in FY 20. For FY 19, the corresponding figure was 23.5%.

In a year heavily impacted by COVID-19, the Group delivered a strong operational result in FY 20/21, with group revenue up 8.8% year-on-year to AUD 5,686 million. Lotteries and Keno revenues came in at AUD 3,206 million, up 9.9% on the previous corresponding period and delivering a record profit result. Turnover of core lottery games (Saturday and mid-week Lotto, Set for Life, and instants) was up by more than 10% across each product offering. Digital turnover grew by 27% and accounted for 32.8% of total lotteries’ turnover for the year, even as the retail network remained the primary channel for consumer traffic. Keno revenues grew by 33.5% year-on-year as the entertainment sector rebounded from the closures of hospitality venues forced in FY 20. Keno digital turnover was up 74%. Commenting on the results, Tabcorp Managing Director and CEO David Attenborough said, “In the face of substantial challenges from the COVID-19 pandemic, our businesses delivered a strong operational performance and double-digit earnings growth. […] The Lotteries & Keno business produced another record profit result driven by strategic game and portfolio development and digital growth. It continued its strong growth trajectory since the Tabcorp and Tatts combination in December 2017.” Tabcorp is expecting to demerge its lotteries and Keno division in mid-2022 following completion of a strategic review.

Europe

Daily new confirmed COVID-19 cases per million people in Europe at end August 2021, 7-day rolling average. (The number of confirmed cases is lower than the number of actual cases owing to limited testing.)

The European response to the pandemic has been varied, both in terms of the damage to various nations caused by the coronavirus and it terms of policy response towards managing the pandemic. France, Italy, Spain, and the UK are among the European countries worst hit by COVID-19, while Germany and Scandinavia (excepting Sweden) have experienced comparative success in combatting the pandemic. Policy responses have ranged from laissez-faire to controlled management; no country in Europe appears to be adopting the ‘zero-COVID’ approach favored in parts of Asia Pacific. Vaccination programs are generally well-advanced across Europe, especially in Denmark, Iceland, and the United Kingdom.

United Kingdom

The United Kingdom has had a mixed response to the pandemic to date. A delay in locking down early in the pandemic, at a time when no vaccines were available, is considered by many observers to have played an important role in the crushing first wave of the pandemic, which led to more than 300,000 confirmed cases and 40,000 deaths in the UK by early August 2020. The force of a brutal second wave of the pandemic, which began in winter 2020 and saw as many as 60,000 daily confirmed cases at one point, was blunted by late February 2021 thanks to an early and aggressive vaccination campaign using the Oxford/AstraZeneca adenoviral vector vaccine. Since May 2021 the UK government has been pursuing a somewhat different approach to managing the pandemic from most of its erstwhile neighbors in Europe, favoring a Swedish-style laissez-faire or ‘live with the virus’ path that has seen daily confirmed cases skyrocket again; nonetheless hospitalizations and deaths have remained comparatively low thanks to the country’s high rate of vaccination.

Record-breaking FY 20/21 results

The pandemic notwithstanding, total UK National Lottery sales broke GBP 8 billion for the first time in the fiscal year through to 31 March 2021. The FY 20/21 record sales of GBP 8,373.9 billion represented an increase of GBP 468.8 million on the previous financial year’s revenues. This marked the fourth successive year of revenue growth for Camelot UK Lotteries Limited, the operator of The National Lottery, following the wide-ranging strategic review undertaken by the company in 2017. This resulted in the best-ever returns to good causes from sales revenues alone, with GBP 1.2 billion in monies awarded for good causes directed to COVID-19 relief.

Like other big national lotteries, the UK National Lottery has traditionally depended heavily on its retail network for its revenues, with in-store retail sales normally responsible for around 70% of total sales. National Lottery retail sales were therefore impacted near the end of March 2020 and into the following month as a result of the UK-wide lockdown measures. Despite the downturn occasioned by the various lockdowns and other pandemic containment measures, the mitigations and swift interventions put in place by The National Lottery – such as the active encouragement proffered by Camelot in supporting the move of their player base to online – led to record sales for the 20/21 fiscal year. The growth in sales was driven by draw-based games, most notably Lotto, with revenues rising by GBP 153.6 million to GBP 4,690.7 million. A new feature introduced in November 2020 sees around a million players win an additional cash prize of GBP 5 for matching two main numbers in a ‘Must Be Won’ roll-down draw. This innovation proved popular with Camelot’s players and has underpinned the growth of Camelot’s flagship Lotto game at a time when sales of numbers games have been declining in many international markets.

Although the UK retail sector was widely disrupted by the COVID-19 lockdowns instituted in the UK in the first half of 2020, with Camelot’s support more than 90% of its 44,000 retail partners continued to trade throughout the various lockdown periods. Nonetheless, in-store sales were down GBP 583.2 million on FY 19/20 in-store sales of GBP 5,447.6 million. Down 18.9% year-on-year at the midway point of 2020, retail sales ultimately recovered strongly in the second half of 2020, resulting in an overall decline in retail sales of 10.7% for the year as a whole. Since year-end 2020, retail sales have recovered to near pre-pandemic trading levels.

Growth of digital

Even as retail sales were depressed by COVID-19 physical containment measures, digital player registrations grew by 2.7 million over the year, amounting to approximately 4% of the entire UK population, resulting in The National Lottery recording its highest-ever digital sales of GBP 3,509.5 million. Year-on-year, digital sales increased by GBP 1,052.0 million, or 42.8%. Within digital, mobile sales grew by GBP 876.4 million to an all-time high of GBP 2,481.9 million, with most sales coming from The National Lottery’s apps. The move to digital occasioned by the decline in retail footfall was underpinned by an accelerated investment plan in the digital channel, which was approved by Camelot’s board in March 2020. The recovery of retail in the second half of 2020 notwithstanding, Camelot continues to see players using The National Lottery’s apps and many punters playing online, reinforcing the view that in the right circumstances, digital channels augment rather than cannibalize the retail channel.

Commenting on the FY 20/21 results, Camelot CEO Nigel Railton said, “In what has been an extraordinarily challenging year, The National Lottery has demonstrated incredible resilience and flexibility to achieve this record performance. These results are a culmination of all of the work we’ve done over the last few years in the areas of brand, games, retail and digital. This, together with our years of experience and longstanding commitment to being a world leader in healthy play, have helped us ensure this vital boon for society when it’s been needed most.” The GBP 1.2 billion raised specifically for COVID-19 relief originated from a commitment made by The National Lottery in late March 2020 to provide GBP 300 million in emergency funding in response to the COVID-19 pandemic. This initial engagement for GBP 300 million in support was subsequently upgraded in April 2020 to a pledge to distribute at least GBP 600 million between all National Lottery distributors. With disbursements now standing at GBP 1.2 billion, this funding is the largest contribution to the UK’s pandemic relief effort outside of government, and has led to a significant increase in positivity towards the National Lottery’s brand.

France

With more than 6.7 million confirmed cases and more than 114,000 deaths, France has been hit almost as badly by the pandemic as the United Kingdom. A first wave of the pandemic in March 2020 was followed by second and third waves in November 2020 and March 2021 respectively, with daily case rates peaking mid-November 2020 at 56,000 confirmed cases per day; as in other countries, the pandemic was managed by a series of lockdowns and similar sanitation measures in the absence of an effective vaccine. France’s vaccination program began on 27 December 2020, after the EU approved the EUA of the Pfizer-BioNTech vaccine. In July 2021 France became one of the first countries in the world to require a health pass (vaccination / negative PCR or antigen test / recovery from COVID-19) to access venues welcoming more than 50 people, including museums, theaters, cinemas, festivals, and sports and leisure centers; following the introduction of the health pass, vaccination rates have lifted considerably.

FY 20 results

In France, a similar story played out for national gaming operator FDJ as for Camelot in the UK, where an H1 2020 decline in revenues was offset by stronger H2 2020 results; momentum then continued to increase in H1 2021, especially from May 2021 onwards. Recall that France was among the more badly hit of major European countries by the initial waves of the pandemic, with a general quarantine being ordered by the French government from 17 March 2020. The general quarantine was lifted 11 May 2020, but closures and travel restrictions continued until 2 June, and a state of health emergency remained in place until 24 July. As a result of these measures, stakes wagered fell by 18.4% overall in H1 2020. Sports betting was particularly badly affected during the first half of 2020, with a year-on-year decline in sales of 40% reported across this product category over the given time periods. The attrition in sports betting observed during the first six months of 2020 was offset by growth of 20% in H2 2020, limiting the decline for the year to 10%, as compared against 2019. Returning to the discussion of the overall results, the gradual recovery during summer 2020 continued throughout the second half of the year, during which time overall stakes grew 2.8% year-on-year, so that the French national lottery recorded a year-on-year decline of 6.8% in stakes across the whole of 2020 to EUR 15,959 million.

Throughout 2020, the retail network demonstrated considerable resilience: even during the height of the first-half lockdowns, 80% of the FDJ’s retail points of sale were permitted to remain open. Sales through the retail network in 2020 totaled EUR 14,424 million, down 10% on 2019 results. In a now-familiar story, sales through retail points of sale were down by more than 20% in H1 2020, but grew to be stable in the second half of 2020. The distribution network held steady at nearly 30,000 points of sale, owing to support initiatives by FDJ and other stakeholders. There was nonetheless a strong growth in the online spend, with digital lottery stakes up over 60% at more than EUR 1.1 billion. Online sports betting activity also posted an increase. Overall, FDJ Group’s online stakes recorded an annual increase of nearly 40% to EUR 1.5 billion, or almost 10% of total stakes.

Commenting on the 2020 results, President and CEO of FDJ group Stéphane Pallez said: “2020 was an unprecedented and contrasted year during which FDJ demonstrated resilience and solidarity. The health crisis had a particularly strong impact on our business in the first half. But the recovery in the second half, combined with the Group’s responsiveness and relevant digital strategy, enabled us to preserve our performance and annual results.”

H1 2021 results

Turning attention to H1 2021, FDJ experienced good momentum, especially from mid-May onwards. On 19 May 2021 outdoor restaurants re-opened in France, while on 9 June certain businesses with indoor patronage re-opened to the public. This included bars, which represent nearly 10% of FDJ’s points of sales. In addition, the national night-time curfew – which had been in place since 17 October 2020 with a check-in time of 6 p.m. – was lifted on 30 June 2021. In view of the disruption to the sporting calendar and the impact of coronavirus containments measures instituted in 2021, a year-on-year comparison with H1 2020 is not possible. However, relative to H1 2019, stakes recorded by FDJ were up by 8.3% to EUR 9.2 billion, thanks to increased point of sale activity occasioned by the reopening of bars together with an uptake in sports betting activity driven by the UEFA EURO 2020 football championship. Lottery games were up 4% on H1 2019 to EUR 6.9 billion, with growth driven by instant games. Draw-based games were stable over the same revenue period, with a 50% decline in stakes from Amigo, a draw-based game popular in bars and taverns, offset by a more than 20% increase in sales for other draw-based products, spearheaded by Loto and Euromillions. The latter benefitted in particular from a long draw cycle in Q1 2021, leading to a Euromillions jackpot of EUR 210 million last February, the highest ever. Sports betting revenues were up 25% on 2019 to EUR 2.3 billion, thanks to a more regular sporting calendar and the EURO 2020 football tournament. The EURO 2020 tournament generated EUR 260 million in stakes for FDJ – a figure comparable to that recorded for the 2018 FIFA World Cup – despite the absence of the French national team from the final phase of the tournament.

Online stakes

FDJ’s online stakes exceeded EUR 1.1 billion through to the end of H1 2021, an increase of more than 70% compared to H1 2020; the figure of EUR 1.1 billion represents 12% of total stakes for H1 2021. Overall digitalized stakes – including online and stakes digitalized at the point of sale, i.e. using a digital service/application for their preparation, prior to registration by the retailer – doubled compared to the first half of 2020, with more than 29% of total stakes placed through digitalized channels. Remarking on the results, Stéphane Pallez said: “The second quarter [of 2021] confirmed a recovery in our business to levels above those recorded before the crisis. Our stakes are increasing, both online and in our point-of-sale network. Over the half-year, we accordingly recorded an increase of nearly 9% in revenue compared with the same period in 2019. Barring new restrictions in response to developments in the health situation, the Group expects to maintain good momentum in the second half and is confident in its business and results prospects in accordance with its responsible gaming model.”

Germany

Relative to the rest of Europe, Germany has had a comparatively good response to the COVID-19 pandemic to date. The first case of COVID-19 was confirmed in late January 2020; by mid-March of that year, German states were mandating school and kindergarten closures, postponing academic semesters, and prohibiting visits to nursing homes to protect the elderly and infirm. Borders to neighboring countries such as Switzerland were closed 15 March, and by 22 March, six German states had imposed curfews. Such measures helped contain the initial wave of the pandemic, and restrictions began to loosen mid-April. A surge in cases during winter 2020 led to a partial lockdown from early November and a tightening of social distancing rules; these measures only temporarily halted a rise in cases. By the end of November 2020, the total number of confirmed cases surpassed one million. A hard lockdown from 15 December made FFP2 (the European equivalent of the American N95) masks mandatory on public transport and in shops; these measures remain in place today. Vaccinations of critical populations such as the elderly began from January. A third wave of infections was driven by the Alpha variant in March 2021; this was broken by early May on the back of reforms in April 2021 that increased the federal government’s powers to respond to the pandemic. With the rise to dominance of the Delta variant, a fourth wave of the pandemic began in late August 2021, with most cases arising in younger people. Currently the country is experiencing around 10,000 new cases per day.

The DLTB

In Germany, like the US and Canada, lotteries are organized at the state rather than federal level. A total of 17 separate lotteries operate in Germany, 16 of which are run by the individual states (Bundesländer). Unlike in North America, however, the 16 state-regulated lotteries operate under the aegis of an umbrella organization, the Deutscher Lotto- und Totoblock (German Lotto and Toto Block, or DLTB). The DLTB ensures the 16 state lotteries operate under standardized rules.

FY 20 vs. FY 19

Germany bucked the trend of many other countries in 2020, with total stakes for FY 20 increasing by 8.8% year-on-year to more than EUR 7.9 billion. Commenting on the results, chair of the DLTB and managing director of Lotto Rheinland-Pfalz Jürgen Häfner said, "The 16 German state lottery companies proved to be crisis-proof and reliable during the 2020 [COVID-19] pandemic. This good annual result shows that our gaming offers are still popular with players – this despite numerous points of sale having to close temporarily during the pandemic.” Mr. Häfner continued, “Many customers compensated for these closures, for example, by submitting multi-week tickets and using our online offerings.”

The most popular product was again Lotto 6aus49, which enjoyed sales of EUR 3.98 billion, accounting thereby for more than half of all wagers. This exceeded the corresponding result for FY 19 by more than 12%. Changes to the game matrix leading to larger jackpots and an increase in the price point to EUR 1.20 helped drive the flagship’s results. Another highlight was the Eurojackpot block game: this multi-jurisdictional game, which is played across 17 countries in Europe, saw stakes rise 18% year-on-year to more than EUR 1.47 billion. Like all block games, Eurojackpot is jackpot-sensitive; a series of long-running jackpot cycles of more than EUR 90 million helped the pan-European lottery game’s performance following a weaker FY 19.

FY 21

The good results for the DTLB continued into H1 2021, with the 16 members reporting that sales collectively rose to over EUR 4 billion in the first half of the year, up 7.9% on H1 2020. Chair of the DLTB, Jürgen Häfner remarked, “Our customers remained loyal to us in the first half of 2021. We are particularly pleased about the significant increase in our long-running LOTTO 6aus49.” Mr. Häfner was referring to the excellent performance of the flagship Lotto 6aus49 game, which saw stakes grow 15.3% over the corresponding revenue period of 2020. “We have managed to make our classic [Lotto 6aus49] fit for the future,” Mr. Häfner said. On the back of the strong H1 2021 results more than EUR 1.6 billion was paid into respective state budgets in the form of taxes and duties. “That means every week around 61.5 million euros flow to the common good. Without this money, many things would not be possible”, proclaimed Mr. Häfner.

New State Treaty on Gambling enters into force

In a separate development, the new State Treaty on Gambling (Glücksspielstaatsvertrag) came into force on 1 July 2021. While the new treaty opens up the market to online casino as well as sports betting, the DTLB has welcomed the treaty’s introduction, saying that it continues to secure the public interest-oriented state lottery monopoly while for the first time also comprehensively regulating online gaming, helping thereby to suppress the illegal online market.

Latin America

Daily new confirmed COVID-19 cases per million people in Latin America at end August 2021, 7-day rolling average. (The number of confirmed cases is lower than the number of actual cases owing to limited testing.)

The COVID-19 pandemic has been particularly bad in Latin America. Brazil remains the world’s second-most heavily impacted nation behind the United States, with more than 20 million confirmed cases. Chile, Peru, and Mexico have also been badly affected by the pandemic, with Peru experiencing the highest death rate of any country on a per capita basis, at more than 6,000 deaths per million people through to August 2021. Progress in vaccinating the region’s populations unfortunately remains slow.

Brazil

The Brazilian national lottery reports that in the fiscal year of 2020 lottery sales were extremely challenging, owing of course to the COVID-19 pandemic. (In Brazil, the fiscal year is the calendar year.) This was especially so during the first phase of the pandemic, where the retail network (physical commercial establishments) was badly impacted by a patchwork of local lockdowns lasting several months over the course of the first half of 2020.

The reduction in lottery sales, identified in the first half of 2020, was owing to the fact that most revenues from the sale of lottery products are raised through physical channels: the point-of-sale network has more than 13,000 units nationwide. As a result of the decreed lockdowns, the lottery network was closed in some periods in 2020. In the second half of 2020, there was an increase in lottery sales, reaching levels of resumption meeting pre-established goals by the company, which occurred as a result of the progressive opening of commercial establishments and the lottery network in the country. Overall FY 20 sales of draw-based games were up 2.6% on FY 2019 draw-based sales, in something of a triumph for the Brazilian national lottery.

With regards to sports betting, national football matches and championships were suspended in certain months of 2020 in most states, which affected bets for lottery products that are based on or are linked to the results of football matches. Consequently, sales of pari-mutuel sports betting products in FY 20 declined 40.7% year-on-year. Overall, sports betting accounted for 0.66% of Caixa’s stakes in FY 19, the most recent year for which consonant figures are available.

The wide dissemination of official electronic betting channels of Loterias Caixa (Loterias Online Portal and the CAIXA Lotteries App), as well as the up-take and satisfactory adherence of the public to Caixa’s official gaming channels, also contributed to the improved results reported in H2 2020. Of particular importance in this regard is that Loterias CAIXA sells lottery products via its highly-regarded Loterias Caixa App on both the IOS and Android platforms, in full compliance with the current policies of use of these platforms. In the first half of 2021, the sales growth trend for revenues coming from electronic channels has been maintained.

The positive trajectory noted for digital sales also carried over to the setting of draw-based games in H1 2021, where sales of draw-based games were up 10.2% in H1 2021, compared to the corresponding revenue period of H1 2020. With the resumption of professional league football matches in particular, sales of sports betting products skyrocketed over the same relative timeframes. While a direct comparison is contra-indicated owing to the disruption to the sporting schedule in 2020, the surge in sports betting sales led to an overall year-on-year increase in sales of 10.8%.

Mexico

Mexico is another country that has been badly affected by the COVID-19 pandemic, with more than 3.3 million confirmed cases and 255,000 deaths to date; the capital Mexico City has been among the hardest hit of the country’s 32 administrative divisions. The development of the pandemic in Mexico has followed a now-familiar path; after COVID-19 emerged in the country in February 2020, a national health emergency was declared on 30 March. Unfortunately the Federal response to the pandemic has been politicized, like in Brazil, with Mexico’s states ultimately imposing a patchwork of measures to curb the spread of disease, such as mask mandates in public spaces, the suspension of in-person teaching in schools and universities, and the enforced closure of entertainment and hospitality venues. Beaches were closed on 1 April 2020. A phased re-opening took place over summer 2020, with many states announcing the re-opening of non-essential businesses from June and the resumption of classes online from August. Mexico’s vaccination program (initially restricted to health-care workers) began early, in December 2020, but was not sufficient to stem the tide of infections: the country experienced a local maxima in cases in January 2021. From March to June 2021 there was a comparative lull in cases; but with the arrival of the Delta variant, daily cases at present are higher than they have ever been. Currently around 25% of Mexico’s population of 127.6 million is fully vaccinated.

Mexico’s national lottery, Lotería Nacional para la Asistencia Pública (LOTENAL), was formed in 1770. Now it is in the process of merging with Pronósticos para la Asistencia Pública (Pronósticos). Once this is complete LOTENAL will offer a full complement of draw-based games, instant games, and sports games. Until then, LOTENAL provides draw-based games only. Currently there is no digital offer.

For calendar year 2020, sales of draw-based games declined 7.9%, as against 2019 calendar year sales, owing in part to the imposition of pandemic containment measures. In contrast, H1 2021 sales of draw-based games were up 63.8% on H1 2020 sales of the same products, reflecting in part the artificially depressed performance of draw-based offerings in the first half of 2020.

While there have been no direct promotions of the lottery’s products in relation to vaccine drives or other aspects of the pandemic to date, proceeds from LOTENAL are currently supporting Mexico’s health sector, in keeping with the lottery’s mission as a governmental entity oriented to social purposes. As such, LOTENAL’s funding for good causes has been of great help throughout the pandemic.

North America

Daily new confirmed COVID-19 cases per million people in North America at end August 2021, 7-day rolling average. (The number of confirmed cases is lower than the number of actual cases owing to limited testing.)

North America’s pandemic response has of course been dominated by the US, which has had among the world’s worst outcomes to date. Indeed, if Mississippi, Louisiana, and Florida were countries, they would each have one of the highest daily case averages per capita in the world, at more than 100 cases per 100,000 people. Canada has generally fared better, particularly since the advent of effective vaccines: at the time of writing, more than 70% of the Canadian population has been vaccinated with at least one vaccine dose.

USA

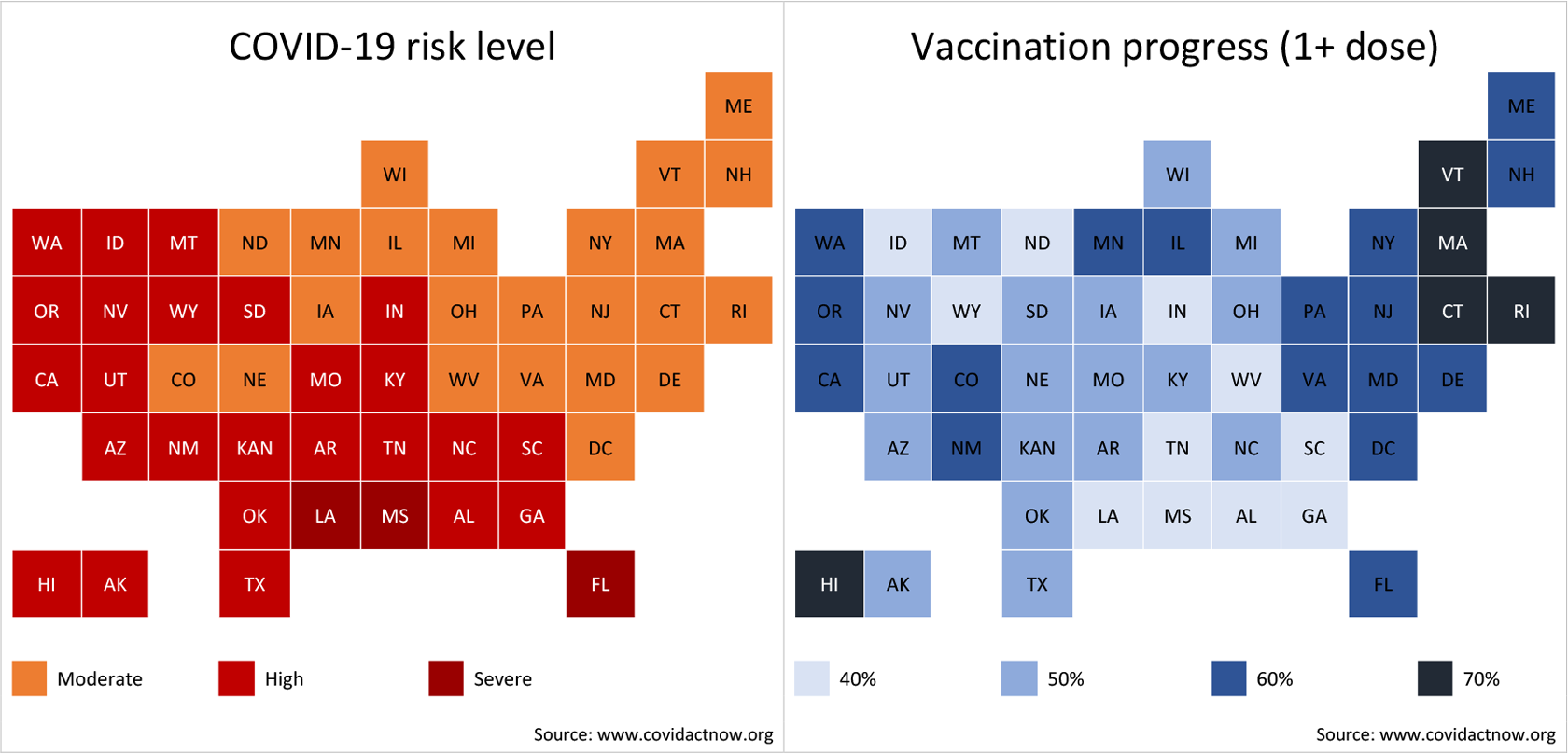

The US remains the country hit hardest by the COVID-19 pandemic, reporting more than 38 million cases of COVID-19 and 630,000 deaths through to the time of writing. A haphazard initial response to the pandemic up to the end of 2020, occasioned (inter alia) by political polarization, a patchwork of federal and state responses including piecemeal lockdowns, together with misinformation and shortcomings in testing permitted largely uncontrolled spread of SARS-CoV-2 throughout the United States through to the beginning of 2021. Following emergency use authorization by the US FDA of the Pfizer-BioNTech and Moderna vaccines in December 2020, a coordinated nationwide vaccination program saw 50% of the US population receiving at least one vaccine dose of a 2-dose regimen by 25 May 2021, blunting the effects of the pandemic thereby through the opening months of 2021 and breaking the causal chains between infection, hospitalization, and death. Vaccine uptake in the US has been uneven, however, with some pockets of the country reaching herd immunity vaccination targets of 80% or more, while other places, especially in hard-to-reach rural areas, have seen vaccinations lag. With the emergence of the Delta variant in 2020, the virus has become resurgent in those parts of the US with lower vaccination rates, most notably the Deep South. As a result, the US is currently experiencing a new wave of COVID-19 cases, largely among the unvaccinated, even as the country is progressively reopening and relaxing restrictions after the various lockdowns and restrictions put in place to manage the pandemic in early 2020. Currently the country is locked in a tight race between vaccination and variants, as evinced by the dual charts of Figure 5.

Figure 5. COVID-19 risk level for the US states vs. COVID-19 vaccination progress as of August 2021.

Vaccine hesitancy in some parts of the United States continues to remain high as disinformation about risks proliferates, with some 40% of the population remaining unvaccinated at the time of writing. In this connection, lotteries have made a novel contribution to overcoming vaccine hesitancy, by offering large cash prizes to be awarded randomly among those who are vaccinated. The first such lottery-based incentive scheme was piloted by the Ohio Lottery in May 2021. This scheme met with some success, and vaccine drawings are now offered regularly by a number of US state lotteries, including Illinois, Louisiana, Missouri, and Oregon.

Results by product category, FY 20 vs. FY 19

The lottery business in the USA was depressed in H1 2020 by the imposition of restrictions on movement early in the pandemic. In response, the national-level multijurisdictional games Powerball and Mega Millions lowered their starting price points and slowed the progression of their top prizes, in response to sales-for-jackpot slowing by about 20%. For the 2020 financial year (ending 30 June for most US lotteries), sales of these volatile games were 61% and 54% (respectively) of their FY 19 values. The lotto-type games of the individual jurisdictions generally fared better. Reports to the North American Association of State and Provincial Lotteries (NASPL), whose membership includes all US WLA-member lotteries together with a similar number of non-WLA-member lotteries, indicate that of 24 jurisdictions offering ‘big’ lotto games (top prizes over USD 1 million, annuitized), eight saw higher sales in FY 20 than in FY 19, while among 42 ‘small’ or ‘cash’ lotto games, 17 showed such an increase. Multi-jurisdictional lotto games defining their prizes as payments ‘for life’ showed sales increases in 12 of the 36 jurisdictions offering them, with aggregate sales 24% higher than in FY 19. However, considering sales of lotto-type games as a whole across all NASPL reporters, the successes of small local games did not compensate for the weakness of the national games: FY 20 sales of lotto-type games were USD 9.9 billion, just 69% of the USD 14.4 billion reported for FY 19.

While lotto games depend on grand scale to make their large and growing top prizes sustainable, games based on matching three or four numbers offer more modest prizes and are not so scale-dependent. Usually, they are offered with draws every day, or twice per day. In the pandemic environment, games of this type grew about 6% (NASPL FY 20/FY 19).

Printed instant games accounted for USD 51.5 billion (about 62%) of US lottery sales in FY 19. This total increased to USD 55.5 billion (67%) in FY 20. This increase in printed instant games (7.7% for the category) largely made up for the shortfall in lotto-type games, with the net effect that sales in FY 20 were 101% of those in FY 19 across traditional product categories (that is, excepting sports betting, video lottery terminals, and the like, offered by a few US lotteries, where volume is not usually reported as sales). Instant games operate at a smaller net win for the lottery than most draw games. Consequently, even though total sales changed little from FY 19 to FY 20, transfers to beneficiaries in FY 20 (USD 23.8 billion) were about 95% of the FY 19 level.

The strength of small numbers games and printed instant games is perhaps surprising, given that these are generally purchased in retail locations that saw less footfall during the pandemic. However, as with other goods, consumers can compensate for fewer store visits by ‘buying ahead’. Given the unchanging nature of the top prizes in numbers and instant games, this is a natural sort of compensation.

The five US lotteries that were able to offer electronic instant games (e-instants, for home or mobile play) all saw spectacular growth in this category (FY 20 / FY 19 = 190%). This was not due simply to the novelty of the category: non-WLA member Michigan Lottery, in 2014 the first in the US to offer e-instants, saw 88% growth in sales from FY 19 to FY 20. Rather, the ability to buy from anywhere has obvious advantages in the context of lowered mobility.

The voluntary closures of gaming and casino venues on Indian reservations in 20 contributed to a major decline in gaming revenues for FY 20. Figures from the National Indian Gaming Commission (NIGC) revealed Gross Gaming Revenue (GGR) for fiscal 2020 of USD 27.8 billion. For fiscal 2019, the corresponding figure from the NIGC was USD 34.6 billion. The USD 6.7 billion decrease in GGR represents a fall in gross gaming revenue of 19.5%. It was a similar story across the US as a whole for 2020, where commercial casino gaming industry revenue declined 31.3% year-on-year.

FY 21

While in FY 20 lottery sales initially fell, then shifted across products and recovered to FY 19 levels, in FY 21 and particularly in the second half of that period there was substantial growth across most product categories. Most US lotteries completed FY 21 last 30 June, and most have reported total sales at record high levels. The Arizona Lottery serves as a case in point. The southwestern lottery enjoyed a record-breaking fiscal year through to June 2021, with sales revenues up 31% year-on-year to USD 1.4 billion (all figures reported are unaudited). The previous sales record had been set just 12 months earlier, in FY 20. The bonanza results resulted in more than USD 260 million in transfers to beneficiaries, including Arizona’s public universities, health services, and local transport networks. Arizona Lottery Executive Director Gregg Edgar said, “The Arizona Lottery and our entire network of valued retailers are grateful to our players who are helping to do so much good in our great state by enjoying our games.” He continued, “The more than a quarter billion dollars that they’ve returned to over a dozen vital programs and services this year are educating Arizonans, housing the homeless, creating jobs, protecting our iconic wildlife and landscapes, and advocating for innocent children who find themselves caught up in the court system.” In addition to transfers to beneficiaries, the lottery paid out more than USD 977 million in prizes and injected US 97 million into the local economy through retailer commissions.

Sales figures have at this writing been compiled by NASPL only through the third fiscal quarter (ending 31 March 2021). Even with partial data, however, great growth in most product categories is evident. Sales of traditional lottery games in the first three quarters of FY 21 were 117% of the corresponding part of FY 20. Printed instant games grew to 119% of FY 20 level. The national-scale games Powerball and Mega Millions recovered, aided by a USD 1 billion advertised jackpot (the second-highest ever) in Mega Millions in January 2021. Aggregate sales of the two games were 134% of the depressed FY 20 levels, though still well below the record sales of the same period in FY 19 (which included both a USD 1.5 billion Mega Millions jackpot and a USD 758 million Powerball jackpot). The less volatile state-level lotto games grew in the first three quarters of FY 21 to 109% of the FY 20 level. Daily numbers games continued to grow, achieving 117% of FY 20 sales. The few US states reporting sales of e-instants reported sales volume double that of FY 20. Also notable was the growth of ‘new game’ content, such as Cash Pop™, which sees players win by matching against a single number in a game matrix of 1 to 15; prize payout is determined by the size of the price point times a randomly chosen multiplier in the range 5 to 250. Introduced by the New Jersey Lottery in 2019, the game has since expanded to Georgia and Kentucky, with other states to follow.

Beneficiary transfers, like sales, are generally reported to be at record levels. More precise conclusions will follow the compilation of results from all jurisdictions.

Canada

Canada’s response to the COVID-19 pandemic, coordinated by the Canadian Federal government and the individual provinces, has resulted in better outcomes overall than in the USA. Although Canada’s vaccination program started later, by May 2021 the percentage of the population fully vaccinated reached 50%, and thereafter exceeded the vaccination rate achieved in the USA. At this writing, 66% of the population has been fully vaccinated (with 74% having received at least one dose) and the rate of new cases is much lower than the peak rate seen before vaccinations became available.

Lottery results, FY 20 vs. FY 19

Sales results are available for all provinces except Quebec, which reports based on GGR. Overall, sales in FY 20 declined only to 98.4% of the FY 19 level. The more volatile national lotto games (Lotto Max and Lotto 6/49) declined by 3% in aggregate. Instant sales were unchanged, while numbers games registered small increases. A decline of 6% in sports betting was largely offset by nearly six-fold gains in Internet games, available in British Columbia, Ontario, and the Atlantic provinces of Canada.

FY 21

NASPL data indicates that for the first three quarters of FY 21, sales of lottery games in the reporting provinces increased to 116% of FY 20 levels. This increase was largely driven by a 30% increase in sales of instant games year-on-year and a further four-fold increase in Internet-only games. The national lotto games gained 5% in aggregate year-on-year, while provincial lotto games gained 18%.

Drivers of change in North America

Despite the great advances made by jurisdictions that can sell lottery products over the Internet, most lottery sales in North America are still made face-to-face at retail. The resilience of lottery sales in the context of greatly restricted retail business was understood to be largely due to even greater impacts of the COVID-19 pandemic on competing gaming venues, such as casinos. Many casinos were closed outright during the first months of pandemic response. Casinos have now largely re-opened; however, we do not see a compensatory slump in lottery sales. Rather it appears that consumer spending on gaming may have increased. For example, in the US state of Maryland, both casinos and lottery are under the control of a single state agency, the State Lottery and Gaming Control Agency. In the financial year just completed (FY 21), the lottery and the casinos together contributed 6.1% more than in their previous record year of FY 19. Although most of the gain came from the lottery, the casinos exceeded their FY 19 performance despite operating at reduced capacity for eight out of 12 months.

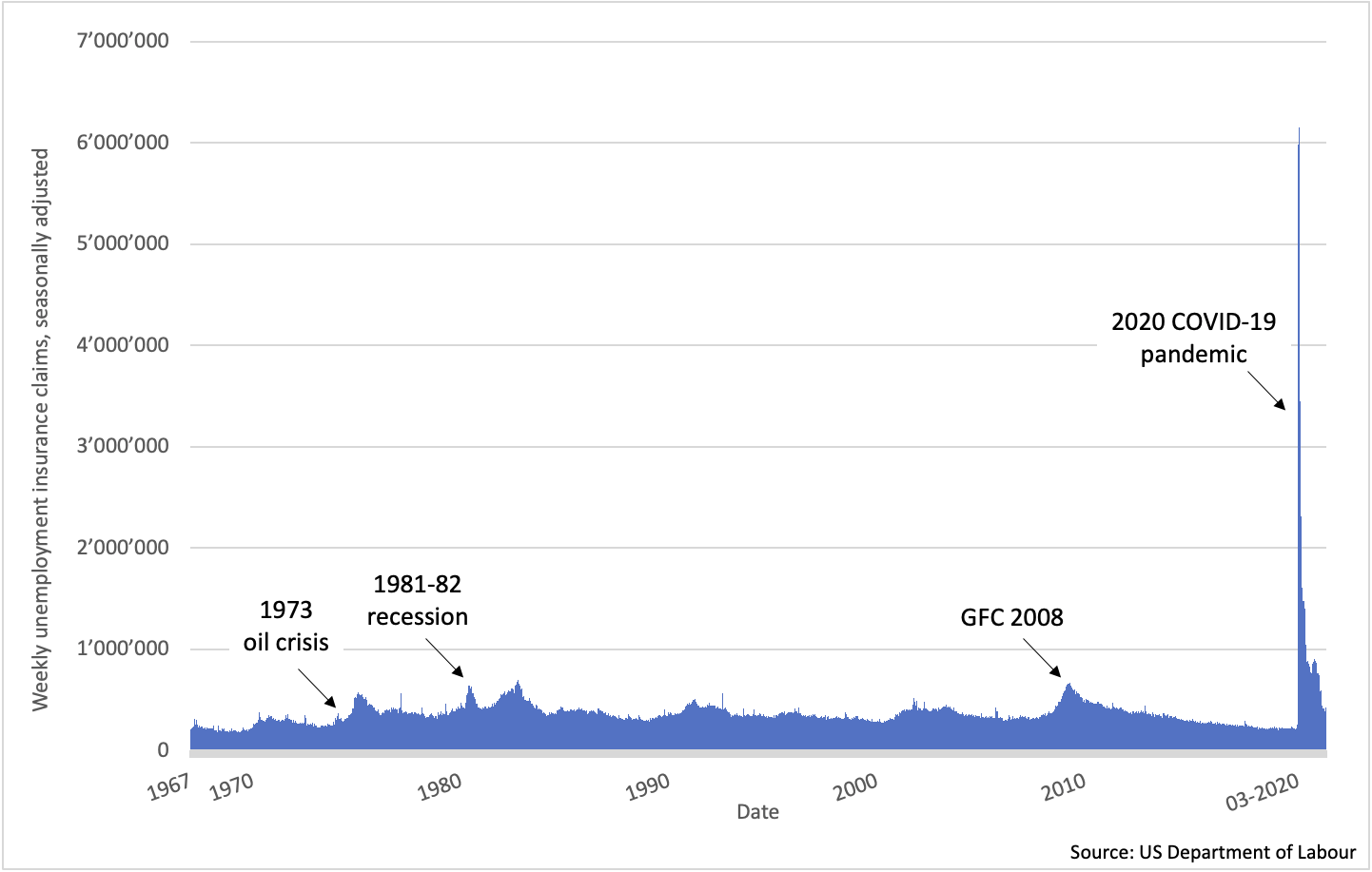

Statistics developed by the US Bureau of Economic Analysis (BEA) indicate that real disposable personal income – that is, income from all sources minus taxes – increased dramatically during the ‘lockdown’ phase of pandemic response (especially the second quarter of calendar 2020), and remains somewhat elevated currently, compared to the immediate pre-pandemic period. In light of US unemployment figures (see Figure 6), this may seem counterintuitive, but personal incomes have been buoyed in many cases by US Federal and State relief programs. Personal consumption expenditures decreased during the lockdown –there were fewer places to spend – before rebounding later in the year. In short, it appears that in the USA at least, people simply have more money to spend. In view of the continuing disruption to many hospitality and entertainment businesses, they also have fewer ways to spend it. Gaming in general, and lottery in particular, are well positioned to capture some of this disposable income.

Figure 6. US weekly unemployment claims (seasonally adjusted), 1967–.

Outlook

With the advent of the COVID-19 Delta variant, and the arrival of further variants expected, most public health officials globally remain of the opinion that the pandemic still has many months to run, even in countries with heavily vaccinated populations. Israel, which has over 60% of its population fully vaccinated, is a sobering case in point. At the time of writing, the country is seeing an upsurge of infections with more than 7,000 new cases daily.

With the development of effective vaccines and economies around the globe continuing to reopen, the IMF paints a rosier picture for the global economy in 2021 and 2022. After projecting a 4.9% decline in real GDP globally for 2020 in April of that year, the contraction in worldwide economic output ultimately came in at a better-than-expected 3.2%. The IMF revised its initial growth projections for 2021 of 5.5% upwards to 6.0% in April 2021, in a move that reflected additional fiscal support in some large economies, a continued vaccine-powered economic recovery in H2 2021, and the continued evolution and adaptation of the global economy to the present pandemic circumstances (including sharply decreased mobility). For details, see Figure 7. The IMF’s improved outlook is reflected in US unemployment figures, which also track the pandemic as a whole: a sharp, riving economic shock followed by a longer road to recovery, underpinned by US Federal and State government unemployment relief and the coordinated vaccine rollout nationwide, as previously illustrated in Figure 6. The improved economic outlook notwithstanding, the IMF cautions however that high uncertainty continues to surround its forecast, with outcomes being dependent on the course of the pandemic, the effectiveness of policy in support of a vaccine-powered normalization, and the development of financial conditions more generally.

Figure 7. IMF actual and projected outlook, 2020–2022, for global, advanced, and emerging economies.

For lotteries and sports betting operators, the history of the pandemic has followed a similar arc to the general economy globally: an initial major dislocation and recovery through to end 2020, followed by a period of increased spend – sometimes to record levels – through the first half of 2021. However, it is not yet clear if the gains made in the market in the six months up to mid-year 2021 will be ‘sticky’. Sustaining current levels of lottery sales may depend upon maintaining lottery as an attractive alternative, as the currently restricted field of entertainment options recovers. Nonetheless, H2 Gambling Capital remains bullish, particularly on lotteries, with their projections suggesting a return to pre-pandemic levels of gross win as early as end 2022: for details, see Figure 8.

Turning to the future, the WLA will continue to report on developments in its continuing coverage of the COVID-19 pandemic and its impact on the lottery and sports betting sector in upcoming editions of the WLA Quarterly Lottery Sales Indicator. By end 2021, a truer picture of the scale and effect of the pandemic on lotteries, sports betting, and gaming should have emerged; the WLA looks forward to reporting on subsequent developments accordingly.

Figure 8. H2GC actual and projected outlook, 2011–2025, for global gross win (lotteries) and global gross win (all gaming).